Are emerging markets worth the risk?

Dr. René Dubacher

Financial Markets

Emerging equity markets have been on a roller coaster ride in recent years. This is not unusual for an inherently volatile part of the global stock market.

Emerging equity markets have been on a roller coaster ride in recent years. This is not unusual for an inherently volatile part of the global stock market.

Emerging Markets

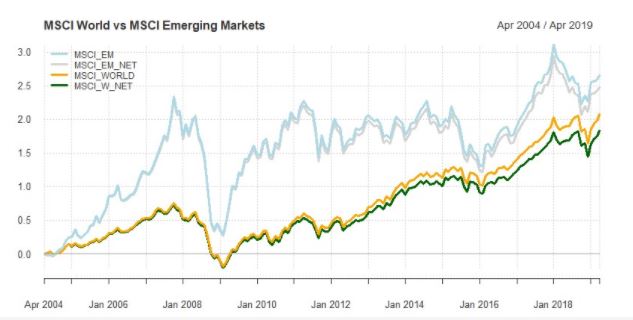

The following chart shows the indexed performance of the MSCI World Equity Index compared to the Emerging Markets Index (both in USD) over the last 15 years. During this period, the emerging markets index achieves a higher performance, with a significantly higher volatility (50%) higher. The outperformance occurred mainly in the period before the financial crisis. Since the beginning of 2009, the performance of emerging markets has lagged the developed world by more than 4% on an annualized basis. This difference is due to the performance of the U.S. stock market, which grew at an annualized rate of 15.3% (S&P 500) in the period mentioned, almost twice as fast as the MSCI Emerging Markets (7.88%).

EMMa vs World

The following table shows the historical performance (4/2004 to 4/2019) as well as the risks and the Sharpe ratio (MSCI in USD):

Return p.a. Risk p.a. Sharpe (RF=0)

EM 9.00% 21.24% 0.42

EM NET 8.64% 21.24% 0.41

WORLD 7.76% 14.52% 0.53

WORLD NET 7.71% 14.52% 0.49

The performance differential in favor of emerging markets improves somewhat if we include the after-tax performance ("net return"), i.e. the performance including the non-reclaimable portion of dividends. Emerging markets are attractive to investors because of strong expected economic growth. The stronger growth of emerging markets is not only due to the fact that the population is growing faster than in other countries. Large parts of Asia are also facing demographic challenges similar to those faced by industrialized nations. They are growing faster primarily because they are increasingly adopting the modern manufacturing techniques of the developed countries and are thus experiencing a process of economic catch-up that is bringing them relatively quickly up to the income levels of the industrialized nations.

The emerging middle classes and changing consumer preferences with newfound economic opportunities are providing new investment opportunities. Gone are the days when investing in emerging markets was all about industry and commodities. Today, it's much more about consumer demand from Millennials, rising e-commerce, and the demand for healthcare and financial services that comes with increasing affluence.

The shift toward consumption in emerging markets is also good news for the global economy, as the U.S. consumer is unlikely to be able to absorb global supply growth in the future. Emerging market consumers and the demand they generate will help Western economies cope with the burden of aging populations and high public debt.

The global economic engine is increasingly shifting east and south, and capital markets will develop in parallel. This bodes well for emerging markets to deliver returns above those of the developed world.

To enable this continued expansion, global capital markets will need to evolve. In this context, it should be noted that the global financial system has not evolved in parallel with the global economy. Emerging markets now account for 40% of global GDP, but only 12% of the MSCI All-Country World Index. Many investors have historically preferred to benefit from emerging market growth through developed market equities, which have significant exposure to emerging markets. Not least because these stocks are more tradable and have lower volatility.

But investment opportunities in emerging markets are changing. Many of the new U.S. trade tariffs target China. China itself is now a strong counterweight to the U.S. because of its trading volume. For a number of Asian countries in particular, China has become the largest export market. In response to the restrictive trade policy of the USA, China has reduced or eliminated tariffs against some important trading partners. These include countries such as South Korea, India and Bangladesh.

Are emerging market equities favorably valued?

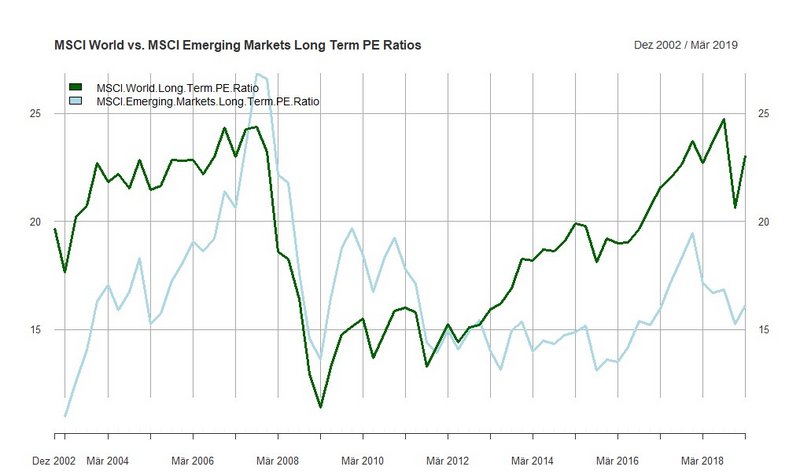

The cyclically adjusted price-to-earnings ratio (CAPE) of a stock market is one of the standard methods of assessing whether a market is overvalued, undervalued or fairly valued. This ratio was developed by Robert Shiller and became popular during the dotcom bubble when he argued (correctly) that stocks were highly overvalued.

EMMA - World - P/E

The share price is what must be paid for a share; the value is what is received for this price. Therefore, there are various ratios that compare the price and the value. The most commonly used ratio is the price-earnings ratio (PE): this divides the price of the stock by the annual earnings per share. Investors usually want to buy a healthy and growing company, especially if the shares can be bought at a low P/E ratio. This way, they get a lot of profit for the price they have to pay.

However, therein lies a problem. In a recession, stock prices fall; but corporate profits also fall sharply. As a result, the P/E ratio may even increase temporarily. If our goal is to buy only when the P/E ratio is low, then this approach gives us a false signal, namely that the market is expensive. But in reality, such moments are the best buying opportunities.

Robert Shiller, Nobel laureate and economics professor at Yale University has calculated a special version of the cyclically adjusted P/E ratio, which is able to solve this problem. Here, the average earnings per share over the last ten years is adjusted for inflation and the current index price is divided by this adjusted earnings. This divides the current price by the average earnings over the last business cycle and not just by one year of bad or good earnings.

The chart above shows the cyclically adjusted P/E ("long term PE Ratio") for emerging market stocks and developed market stocks. While the value for the MSCI Word is close to the long-term high, this is not the case for the emerging markets. The value is in the lower third of long-term valuations. Therefore, the long-term expected returns are very much in favor of emerging markets.

The impact of the US dollar on emerging markets

The US dollar, represented by the US dollar index (DXY) and emerging market equities are historically negatively correlated. That is, when the US dollar falls, emerging markets rise and vice versa. Historically, many emerging markets have been indebted in USD. A rise in the US dollar means that servicing foreign debt, measured in local currency, becomes more expensive.

Borrowing in foreign currency, on a larger scale, is almost exclusively an emerging market phenomenon. Justified by the underdevelopment of certain local capital markets and typically associated with low domestic savings. The second reason is the negative correlation between the U.S. dollar and commodity prices. With some important exceptions, such as China, India and Turkey, emerging markets are net exporters of commodities.

The following chart illustrates the relationship between the U.S. dollar and relative performance of emerging markets. Shown is the cumulative performance difference between emerging market equities and developed market equities. If the upper curve rises, we experience a phase of outperformance of the emerging markets and vice versa. The green curve shows the inverse of the DXY index, which has also been scaled by a factor of 2. The positive relationship of these two curves is obvious. It is statistically significant and in the simple regression the change in the DXY index can explain about 15% of the performance difference between MSCI World and MSCI Emerging Markets.

MSCI World/EMMA vs DXY

The US Fed's monetary policy changes in the first quarter of 2019 had a significant impact on relationships. The strength of the dollar in 2018, particularly in the second and third quarters of the year, exerted strong downward pressure on emerging market assets. The rise in the U.S. dollar was driven by accelerating U.S. growth, which in turn supported additional strengthening. Since January 2019, the Fed has been "patient," according to statements by Powell. Accordingly, the appreciation of the US dollar has also come to an end, which will support the relative performance of emerging markets in the coming months.