Bonds are more attractive than they have been for a long time

Lukas Haas, CESGA

Financial Markets

Bonds are more attractive, also relative to equities, than they have been for a long time. They can once again better fulfill their traditional function in income-oriented strategies.

Bonds are more attractive, also relative to equities, than they have been for a long time. They can once again better fulfill their traditional function in income-oriented strategies.

Bonds are more attractive than they have been for a long time

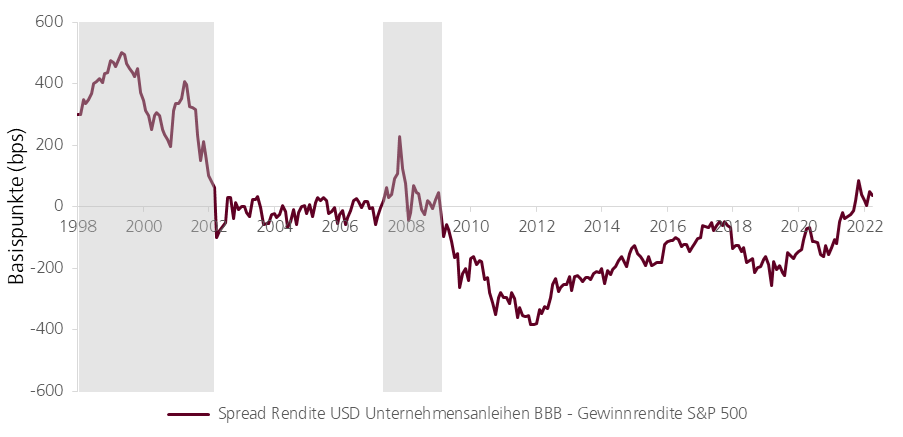

The yield differential between USD corporate bonds in the BBB rating range and the S&P 500 earnings yield (stock earnings per share divided by stock price) is in positive territory for the first time since the global financial crisis in 2008. The average yield on BBB corporate bonds is currently 5.5%, +0.4% or 40 basis points (bps), compared to an earnings yield of 5.1% on the S&P 500. (One basis point equals 1% of 1%, or 1/10,000).

Attractive Bonds

Attractive Bonds

Sources: Swiss Rock, Bloomberg

This yield difference - sometimes referred to as the equity/bond spread - is typically negative, due to the higher risk of equity investments compared to bonds. The spread moves into positive territory when a lot of ("speculative") money flows into the equity markets: Prices rise and this is associated with higher valuations, such as rising price/earnings ratios ("P/E"). For example, the spread was clearly positive during the so-called "dotcom boom" in the late 1990s/early 2000s. The spread was also positive shortly before the global financial crisis in 2008.

The earnings yield of equities using the S&P 500 as an example is currently lower than the bond yield of comparable quality (USD, BBB rating). It is not plausible for us why the market does not currently demand a risk premium for equities compared to bonds. In other words: a - broadly diversified - investment in (corporate) bonds is more attractive than it has been for a long time for three reasons:

- Significantly higher interest rates or a clearly higher absolute interest rate level

- Equally clearly higher risk premiums for non-government bonds

- The valuation of bonds compared to equities is also attractive

Bonds with an air bag

Bond yields depend on movements in the yield and credit curves. The significant rise in yields since just over a year ago has created a risk cushion that can protect against further interest rate hikes and rising credit premiums. Such a "buffer" has no longer existed in recent years due to unrestrained expansionary monetary and fiscal policies with absurdly low, sometimes negative interest rates. Bonds can once again fulfill their function in income-oriented investment strategies much better. A good thing.