Focused growth funds: easy come, easy go

Dr. Martin Schlatter, CEFA

Financial Markets

The violent rotations between different investment styles has struck fear into the hearts of investors in growth funds since the end of 2021. With the surprising rise in inflation, investors' focus has shifted away from growth stocks to spurned value stocks.

The violent rotations between different investment styles has struck fear into the hearts of investors in growth funds since the end of 2021. With the surprising rise in inflation, investors' focus has shifted away from growth stocks to spurned value stocks.

The chart below shows the relative development of returns of value and growth strategies for the two regions Europe and North America.

When the line rises, value stocks outperform growth stocks and vice versa. After the technology bubble burst in early 2000, value stocks outperformed growth stocks in both regions until 2005 / 2006. In Europe, they outperformed growth stocks by around 70% and in North America by around 60%.

For the next 15 years, growth stocks more or less dominated the market. There has only been a major countermovement after the financial crisis. During these 15 years, growth stocks outperformed value stocks by more than 100%.

Returns of value stocks vs. growth stocks in Europe & USA

Returns of value stocks vs. growth stocks in Europe & USA

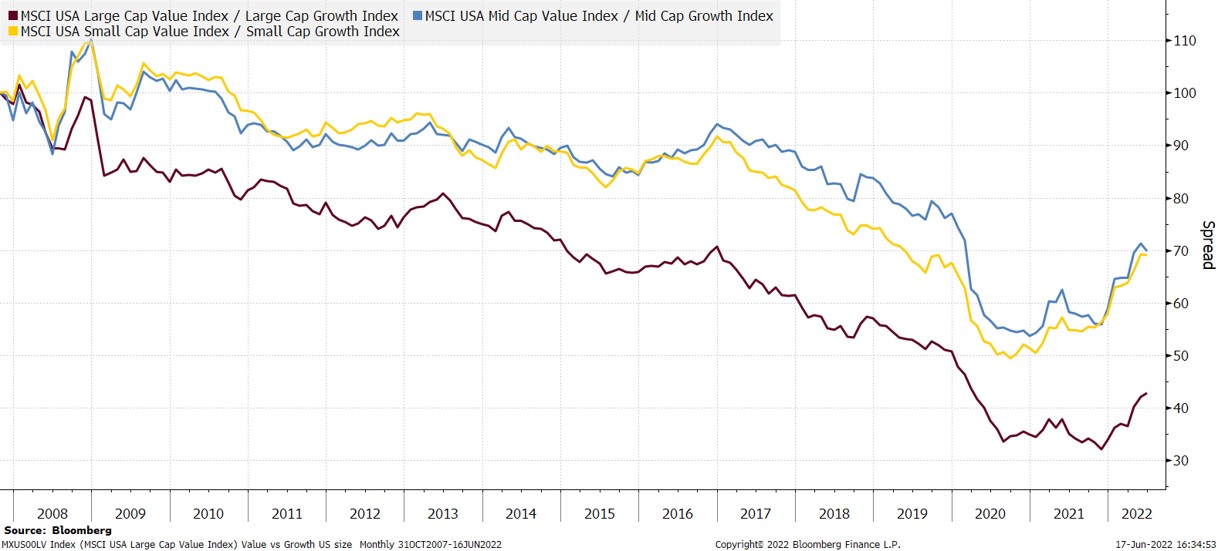

Also interesting is the analysis along the capitalization classes. For the US, the next chart shows the same Value /Growth analysis for large-, mid- and small-capitalization stocks. Clearly, the excess return was even more pronounced for large-cap stocks than for mid- and small-cap stocks. There greets once again the extreme return of the FAANG stocks (Facebook (Meta), Amazon, Apple, Netflix and Google (Alphabet)). In recent years, these stocks, together with Microsoft, have clearly dominated the US market.

Value / Growth: large-, medium- and small-capitalized

Value / Growth: large-, medium- and small-capitalized

Of course, this has not gone unnoticed by fund managers and investors. Many global funds have focused on this segment and made targeted investments in the largest growth stocks.

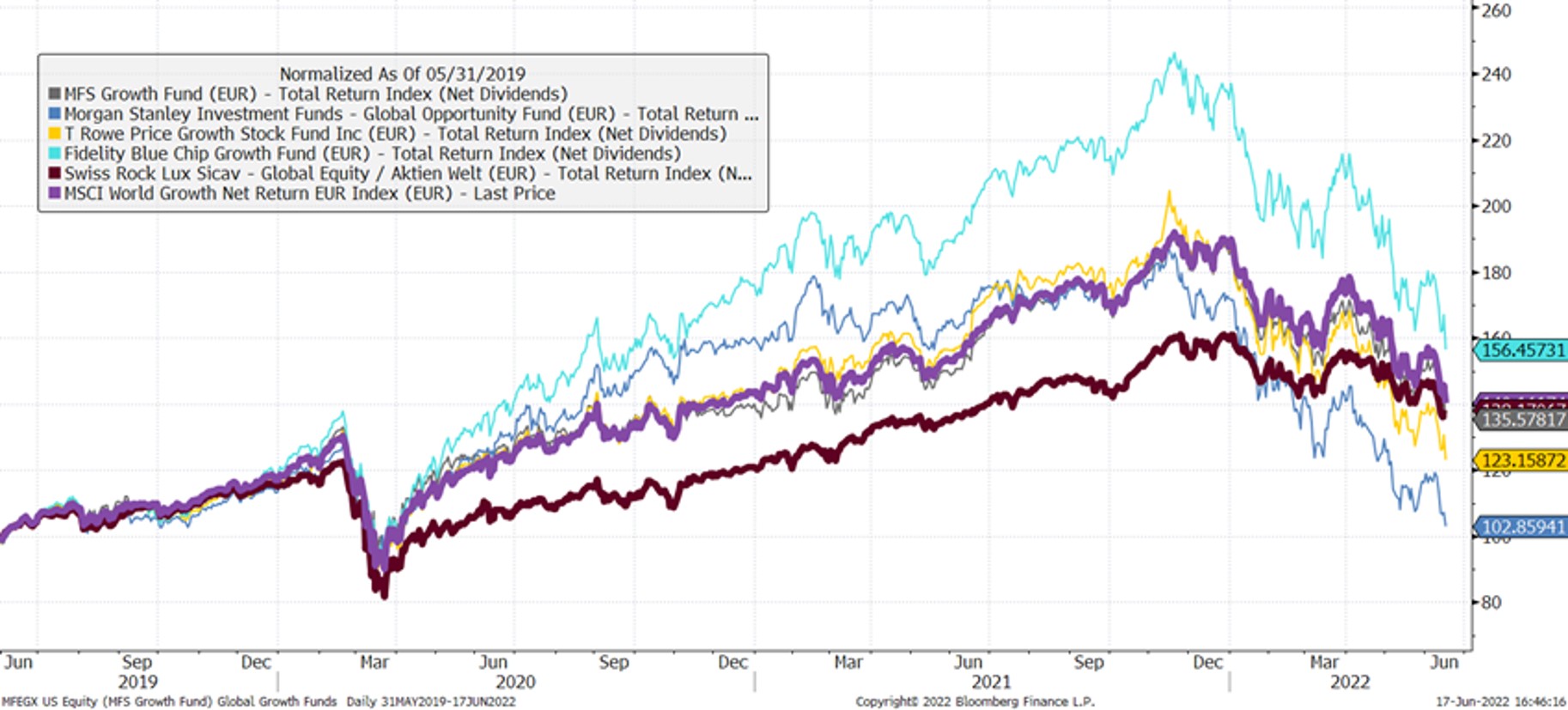

For the next chart, we have picked out the four largest funds from Morningstar's "Global Growth Funds" universe and look at their performance over the last three years. The majority of these funds manage well over $10 billion. We compare the returns on the one hand with the MSCI World Growth Index and on the other hand with the Swiss Rock Aktien Global fund, which implements a balanced strategy between growth, value and quality in the portfolio.

As Morningstar's categorization suggests, the Growth funds move very similarly to the MSCI Growth Index, so they map well to a global growth strategy.

This strategy has provided very nice returns in a falling interest rate environment through the fall of 2021. However, the strategies do not cope as well with the much changed inflationary environment thereafter.

Growth funds vs. multi-factor global equities fund

Growth funds vs. multi-factor global equities fund

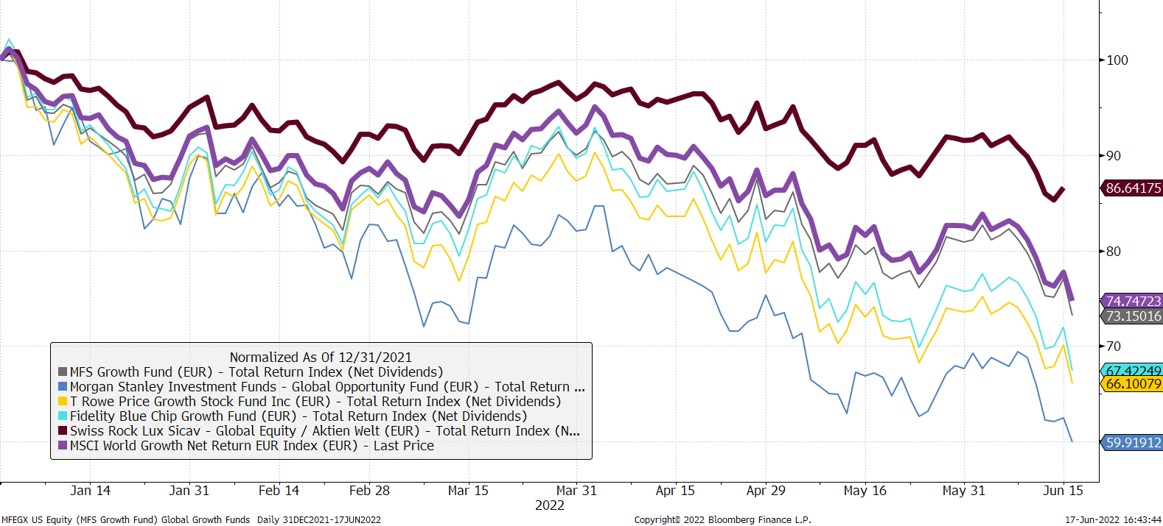

The entire excess return of the growth funds vanished into thin air in the first half of 2022, a very painful correction and only in a very short time.

In comparison, a more balanced equity strategy, which not only focuses on US growth but also takes into account the other investment styles such as substance and quality, has achieved a similar cumulative return with much less volatility. In the last six months, the outperformance compared to growth funds has been striking, as the following chart shows:

Swiss Rock Global Equity fund vs. Growth funds

Swiss Rock Global Equity fund vs. Growth funds

It can now be argued that growth funds can also recover compared to a much better diversified equity portfolio. That is indeed the experience of the last twenty years, but during that time interest rates knew only one direction, namely down. Given the completely changed interest rate environment and the spectacular rise in inflation - especially abroad - the question is what will happen in the next ten years?

For us, the answer is clear: we clearly prefer a less focused strategy that is more robustly positioned against unexpected developments. This is only associated with lower volatility.