Real added value with Swiss equities

Dr. René Dubacher

Financial Markets

More than a hundred years of empirical evidence indicates that equities, while highly volatile in the short run, reward investors with a higher return over bonds and cash in the long run. This return differential, the so-called equity premium, is the reason most investors invest in a diversified equity portfolio.

More than a hundred years of empirical evidence indicates that equities, while highly volatile in the short run, reward investors with a higher return over bonds and cash in the long run. This return differential, the so-called equity premium, is the reason most investors invest in a diversified equity portfolio.

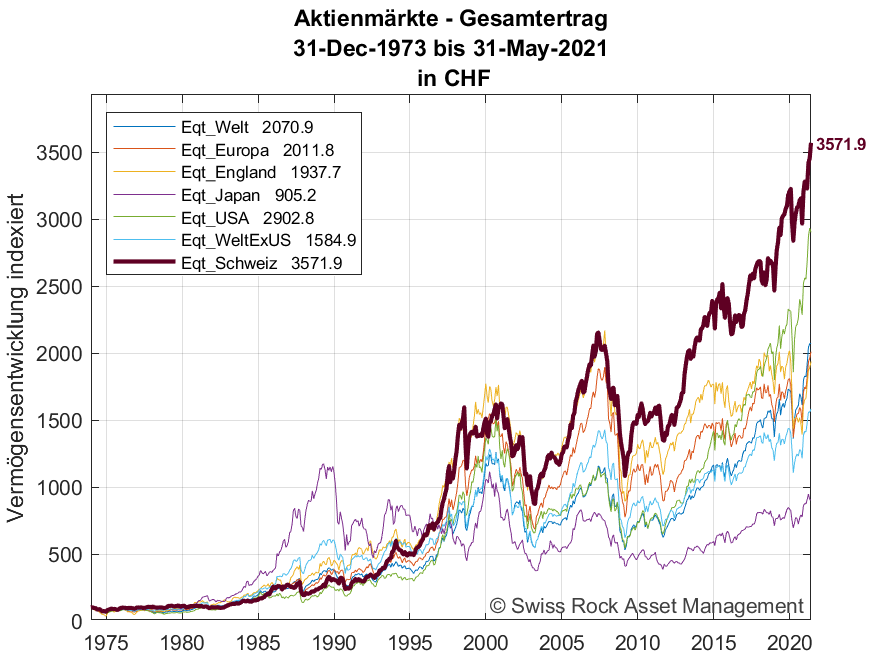

Swiss stock market is world class

More than a hundred years of empirical evidence show that while equities are highly volatile in the short term, they reward investors with a higher return than bonds and cash in the long term (for Switzerland, see e.g. Pictet&Cie: Performance of Equities and Bonds in Switzerland 1926-2020). This return differential, the so-called equity premium, is the reason why most investors invest in a diversified equity portfolio. An increasingly popular way to generate the equity premium in practice is to track a broad capitalization-weighted stock market index, which serves as a good approximation for the theoretical stock market portfolio. Such a passive investment approach allows investors to realize the equity premium at a low cost.

As the following chart shows, Switzerland leads the world in terms of performance compared to other equity regions.

Cumulative performance in CHF

«Home Bias» Criticism Runs into the Void

A popular investor criticism is the so-called "home bias" of many female investors. According to this, the proportion of Swiss equities in a global equity portfolio starting at around 4% is (much) too high. This is typically justified by stating that the weight of the Swiss stock market according to the MSCI World Universe is 3.7%. This oversize of the domestic stock market is typically pejoratively substantiated. But even a frequently expressed opinion does not necessarily have to be correct. A look at the historical data is enlightening and the XXL claim of the domestic stock market is wrong for two reasons:

- As the above chart shows, Switzerland is the world's top performer compared with other equity regions. A higher weighting of the home market seems to be empirically well justified

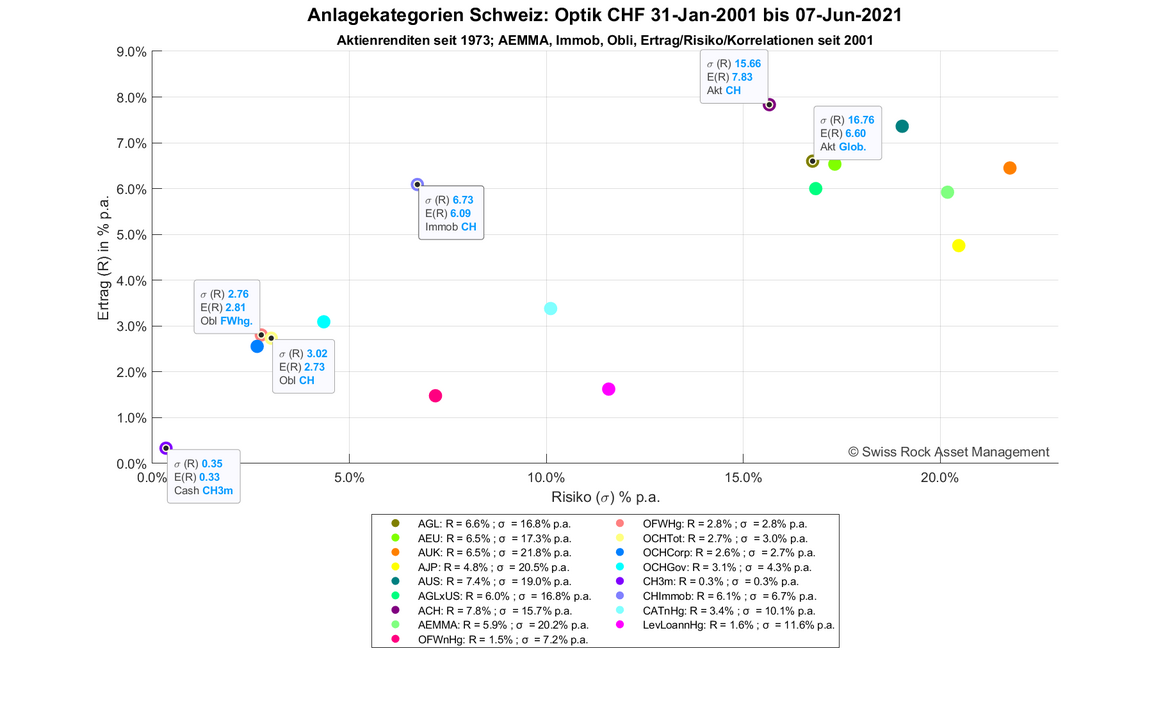

- This extremely pleasing finding, which is robust in the historical course of the stock markets, becomes even more attractive when it can be stated that the risk of the Swiss stock market is still very low in a cross-comparison. As the following return/risk graph shows, the Swiss equity market is at the top left of the cloud of points for equity strategies (to the right of 15% risk), i.e. highest return with lowest risk

X-axis: risk p.a.; Y-axis: return p.a.

«Enhanced Indexing» in the Swiss Stock Market

Passive investing amounts to each investor investing in thousands of individual stocks. These thousands of investments together should earn the equity premium. But does each of these individual stocks really help them earn the total equity premium? Wouldn't it make more sense to invest in a minimum volatility portfolio that can generate the same expected return premium over time with less risk? The literature on minimum volatility strategies shows that there are many successful approaches to constructing portfolios that are less risky than a broad capitalization-weighted market index. For these reasons, it is clear that passive investing in a broad market index cannot be a best practice.

So what assumption would justify passive investing in a broad capitalization-weighted market index?

How can we further optimize the benefits of Swiss equities with a risk-controlled active approach?

Assuming that the Capital Asset Pricing Model (CAPM) holds, it can be shown that the market portfolio is indeed the optimal choice for investors. The CAPM postulates that the expected return on a stock is proportional to the level of systematic risk, or beta. In other words, a stock that is half as risky as the equity market portfolio should receive only half the equity premium, while a stock that is twice as risky as the equity market portfolio should receive twice the equity premium.

Passive investing according to a broad capitalization-weighted index is thus justified, assuming that the CAPM works. Empirically, however, the model has a very poor track record. Studies testing the CAPM's predictions against real data have failed to find a positive relationship between systematic risk and stock returns. The actual relationship appears to be very flat or even negative, i.e., as a tendency, riskier stocks generate lower rather than higher returns.

While systematic risk has proven to be a poor predictor of future expected stock returns, several other stock characteristics, such as size, valuation, momentum, and quality characteristics of a stock, have proven to be powerful indicators of future expected returns. Models that incorporate a combination of such factors have effectively replaced the theoretically elegant but empirically disappointing CAPM. Examples of such models are the three-, four- and five-factor models of Professors Fama and French and other factor models such as those used by Swiss Rock.

My name is Normal Consumer, Otto Normal Consumer

To invest passively in the capitalization-weighted index is to implicitly assume that a model such as the CAPM applies, and that the factor premia observed in the historical data are either not exploitable or will not come into play in the future. Index investors have the additional characteristic of an "average Joe" who does not deviate from the average.

Passive investing, then, means putting a significant portion of the portfolio into stocks that have a negative expected premium. If investors don't want to passively suffer from stocks that just cost them money, what can they do instead? One alternative would be to passively invest in all stocks except, say, the 20% of stocks with the least attractive factor characteristics.

Factor characteristics are not constant, however, but are constantly changing over time. Specifically, this means that the unattractive stocks differ each month. The changes are not drastic, but the portfolio still needs to be managed. Thinking about this problem, one quickly comes to the conclusion that not only should the 20% unattractive stocks be avoided, but the proceeds should also be invested in the 20% most attractive stocks. Swiss Rock's "Enhanced Indexing" approach, which we refer to as Swiss Equity Index Plus, follows exactly this strategy.

Cumulative additional return 4-factor model (relative to index)

The chart shows the additional return generated in real terms compared to a mechanical index replication, which could be realized with the disciplined and patient implementation of our Swiss multi-factor model for clients.

There is a broad scientific evidence that diversified factor investments generate - compared to the market - a positive additional return in the long run; this is also referred to as "risk premiums". Premiums are the reward for taking on additional risk, for absorbing losses in bad times, and for the cyclicality of factor returns. Experience and financial research show that the stock market offers investors who are willing to deviate from "Joe Normal" (also: who consciously take on risk in a controlled manner or are capable of taking on risk) the opportunity to generate an attractive additional return by taking on factor risks in a controlled manner compared with a passive investment strategy.