30 years of SMI - time for a pit stop

Dr. René Dubacher

Financial Markets

30 years ago, the then Association of Swiss Securities Exchanges published the Swiss Market Index (SMI) for the first time. SIX is celebrating the anniversary of what it describes as Switzerland's most important equity index and at the same time opening a special exhibition at the Swiss Finance Museum.

30 years ago, the then Association of Swiss Securities Exchanges published the Swiss Market Index (SMI) for the first time. SIX is celebrating the anniversary of what it describes as Switzerland's most important equity index and at the same time opening a special exhibition at the Swiss Finance Museum.

Stock index SMI

Reason enough for us to take a critical look at the SMI and its use. In the article "On the development of the new Swiss Market Index (SMI) as the basis for Swiss index contracts", Ricardo Cordero, Heinz Zimmermann and the author of this blog described in detail the approach taken in the course of the product development, which was carried out for the then SOFFEX. Based on this analysis, SOFFEX decided to use a capitalization-weighted 24 index as the basis for the index products and to name it the Swiss Market Index (SMI).

The launch of the SMI index was a success story: In addition to tracking the 24 stocks, the index also served, in particular, as an underlying for derivatives, enabling all market participants to trade futures contracts with low bid-ask spreads. In parallel, the SMI index also serves as a benchmark for active and index-based investing.

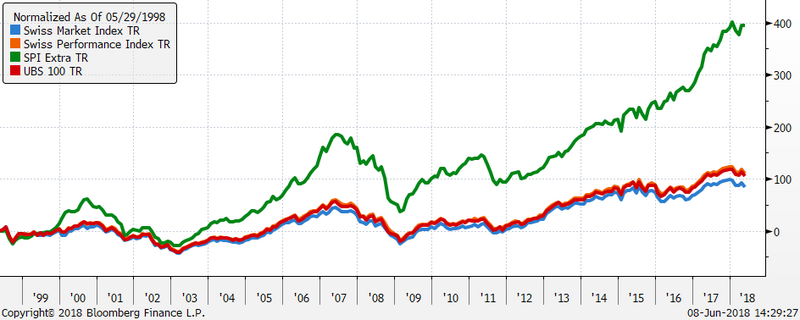

Over time, the term SMI came to be equated with blue chips or "large cap" stocks for the Swiss equity market. Many institutional investors were and are of the opinion that no additional performance can be achieved in the standard stocks defined in this way with active portfolio management and limit(ed) themselves to low-cost index replication. If one compares the overall performance of the SMI (incl. reinvestment of dividends) with that of all other stocks (SPIExtra), which together represent the Swiss stock market (SPI index), the picture is bleak. The currently celebrated SMI index achieved an annualized performance of 3.10% over the last 20 years compared to 8.3% for the SPI Extra. A crushing difference.

Index Price change Total-Performance Yield

(immer inkl. Dividenden) in % in % in % p.a.

SMI: Swiss Market Index 10.46 82.55 3.05

SPI: Swiss Performance Index 110.71 110.71 3.79

SPIex: Swiss Perf. Index Extra 394.60 394.60 8.31

UBS 100 Index 105.99 105.99 3.68

Overall performance since 1998 in comparison

SMI share index compared to other Swiss indices

There may be many reasons for the difference in performance: the underperformance of pharmaceutical stocks, the financial crisis and its impact on the banking sector, the widely varying weighting of sectors, or the absence of the technology sector in the SMI. As a benchmark for large-cap stocks, the SMI index, with a coverage of around 80% of the market capitalization of the entire market, is insufficient. For an investment benchmark, the number of index stocks and the market coverage is far too small. In the context of institutional investors, the low number of stocks cannot be justified by a lack of liquidity either, because these investors have no need to shift millions of shares every minute. The UBS 100 Index comes much closer to the requirements of a large or larger capitalized benchmark index. It covers a high 97% of the total market capitalization. The current 100th stock (Autoneum) has a market capitalization of 1.2 billion Swiss francs, with a daily trading volume of 4 million.

Internationally, "large cap" indices are established with approximately 90% coverage of the total market capitalization. This would correspond to the largest 50-60 stocks in the SPI index, a significantly higher number of stocks than in the SMI index in any case.

It would be desirable for SIX to review the construction logic of the index after 30 years and to calculate a benchmark index for blue chips that increases the attractiveness of large caps, meets international criteria more fairly and can be used as a stable core of a Swiss equity portfolio.