Emerging Market Equities (EMMA) or Asia+ ?

Dr. René Dubacher

Financial Markets

Skeptics often talk about investing in emerging markets as nothing more than an Asia-plus strategy, since Asia makes up 80% of the index. As is all too often the case in media financial discourse, opinions are quickly expressed; this says nothing at all about the substance of the content.

Skeptics often talk about investing in emerging markets as nothing more than an Asia-plus strategy, since Asia makes up 80% of the index. As is all too often the case in media financial discourse, opinions are quickly expressed; this says nothing at all about the substance of the content.

Yes, the share of Asia is above average. Nevertheless: we are convinced and show in the following that investments in all emerging markets are significantly more interesting than Asia alone.

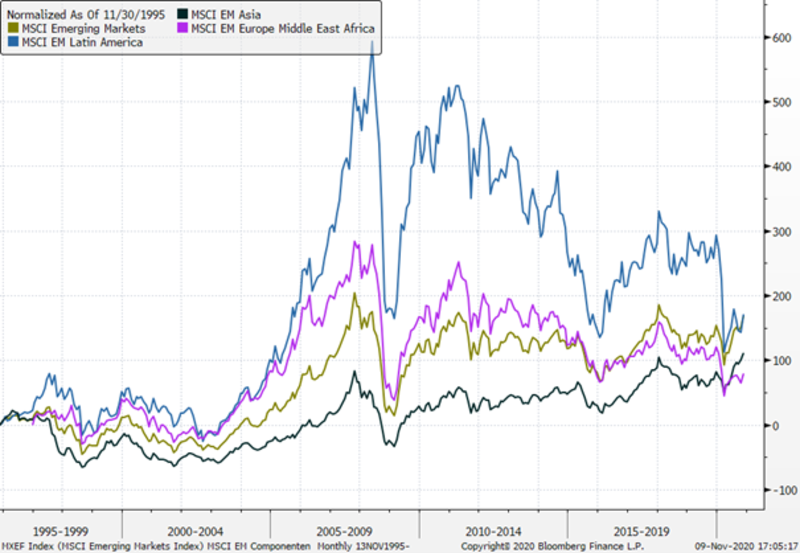

In a first step we compare the cumulative performance of the three main regions of the MSCI Emerging Markets Index. These are "Emerging Asia", Latin America and EMEA (Emerging Europe, Middle East and Africa).

Emerging markets equities vs. Asia+

Source: Bloomberg, MSCI

What has driven the performance of the emerging markets asset class over the past 25 years is not emerging Asia, but emerging EMEA and Latin America. Once again, the positive impact of diversification in emerging market investing comes through loud and clear. Diversification means better returns per risks taken; it is not without reason that diversification is the only free service offered by financial markets. Of course, the dominant weight of Asia remains a fact. As the chart shows, it has long been difficult to generate good equity returns in this region, despite high economic growth. We believe the main reason for this is unfriendly shareholder policies. Some Asian managers still see dividend payments as a sign of weakness, although this is slowly changing with generational change.

In South Korea, for example, the payout ratio of corporate profits has risen from a meager 15% to 30%. However, this is still lower than in Taiwan (60%) and well below the global average of 40%.

A striking number of companies in Latin America are still achieving good returns despite lower growth figures on the continent. The reasons for this are attributed to the Anglo-Saxon approach to business. Compared to Asia, Latin American companies are run much more in the interest of shareholders. While the situation in Asia is improving, too often equity is seen as "free money" and managers fail to make balance sheets more efficient.

Latin America has suffered more than other equity markets from the Covid-19 pandemic. The collapse of commodity prices and the protectionist trade policies of the U.S. government have played their part. Still, the region is visibly improving. Over the past decade and a half, Latin America's higher education enrollment rate has risen to 45% (World Bank). Even in less developed regions with impoverished populations, higher education enrollment rates have risen to as high as 25% in 13 years. As a result, people have become increasingly familiar with economic and financial concepts. But, of course, success in business does not depend on a bachelor's degree.

Latin America's demographics favor innovation. According to the latest data, the median age of Latin American people is 31. This means a higher concentration of Millennials and Generation Z, who are statistically more prone to innovative ideas and experimentation.

As Latin America is undergoing economic development, wages and salaries are still quite low: according to the OECD, the last eight countries in the world in terms of wages and salaries are in Latin America. This directly means that companies can hire qualified talent at an affordable cost, making their projects more feasible.

Although neglected for decades, Latin America is now one of the most promising regions for investment, with a growing number of FinTech startups and VC investors. With an index weight of just over 7% of the MSCI Emerging Markets, the share is small, but offers the possibility of repeat outperformance in the future. In addition to the aforementioned educational and demographic factors, the strengthening economic growth, commodity prices recovering from historic lows, and the expected less protectionist stance on trade issues from the new U.S. administration should help.

To conclude in the words of Harry Markowitz: "Diversification is the only free lunch in investing" The MSCI Emerging Markets Index remains the better choice for long-term investors.