Risk Rally in November

Dr. René Dubacher

Financial Markets

The SPI rose by 8.41% in November, the best November performance since the index has been calculated and the highest monthly performance since the end of the financial crisis (June 2009). The SPI thus lagged behind the MSCI World Index of 11.45% in Swiss francs.

The SPI rose by 8.41% in November, the best November performance since the index has been calculated and the highest monthly performance since the end of the financial crisis (June 2009). The SPI thus lagged behind the MSCI World Index of 11.45% in Swiss francs.

Performance SPI Index

Quelle: Bloomberg

Most of the performance was achieved in the first few days, when both Pfizer/Biontec and Moderna were able to announce effective vaccines against Covid-19. Stock markets were further boosted by the outcome of the U.S. elections, the victory of Joe Biden and the fading of the Democrats' hegemony in Washington.

In Switzerland, the "value" sectors of financials (+21.78%) and industrials (+10.87%) were the best performers along with consumer cyclicals (+27.52%), while the defensive sectors of consumer staples (-1.36%), utilities (1.64%) and healthcare (7.38%) were the worst performers.

Value had its best month in a long time. At the same time, all other styles except small cap ("Size") posted losses, with Momentum, Low Risk and Growth suffering the most.

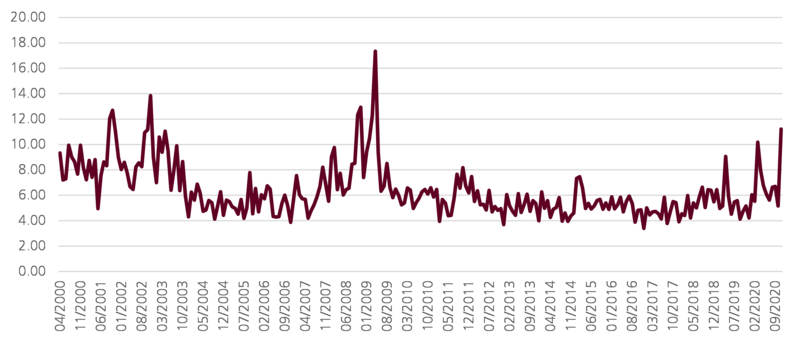

The chart below shows the cross-sectional dispersion ("Dispersion") of returns for the largest 100 stocks in the Swiss Performance Index SPI. This is calculated as the simple, unweighted standard deviation of the monthly returns of the relevant stocks ("trimmed" at 1%).

Cross-sectional diversification Swiss equities

Stock return dispersion can be viewed as a measure of the directional similarity of stock returns over a given period. Unlike traditional measures such as correlation and volatility, return dispersion provides an aggregate measure of common movement in a portfolio for a given period. High directional similarity in returns means that they are primarily driven by macro factors rather than stock-specific factors. Since the 08/09 financial crisis, macro factors have become significant and increasing drivers of stock returns.

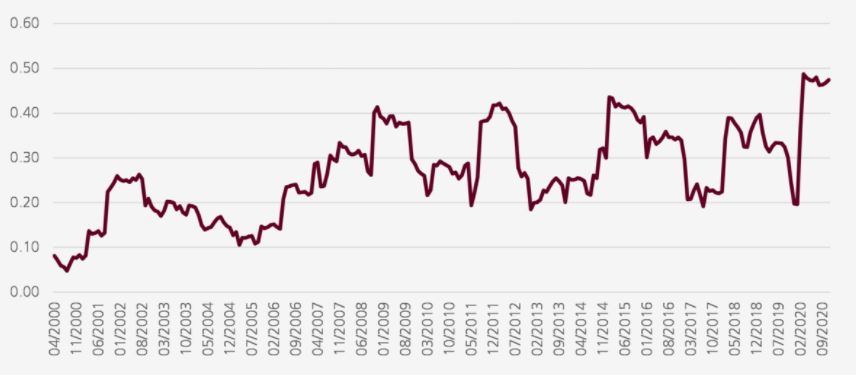

A second way to examine market concurrency is to look at the average pairwise correlation of stock returns. To gauge the extent to which broad market indicators, as opposed to stock specifics, are moving markets, we look at the average pairwise correlation between stocks, using a rolling twelve-month weekly return, in the chart below. When pairwise correlations are high, it suggests that macro indicators contribute more to stock returns.

Correlation Swiss Equities

Since the last financial crisis, both the Fed and the European Central Bank have supported the markets. The term "Fed put" represents investors' belief that the central bank will intervene - as it has for the past two-and-a-half decades - in any crisis. Famously, Mario Draghi said at the time of the euro crisis when he promised that the ECB would do "whatever it takes."

With so much political backing and supportive central bank actions for rising markets, market corrections - regardless of their cause - become a buying opportunity ("buy on dips"). MaW, the behavior of market participants can best be characterized by the acronym "FOMO" ("Fear of Missing out"), the risk of missing another lucrative buying opportunity. Such behavior can lead to a remarkable disconnect between the markets and the real economy in certain market areas. The dangerous consequence of this is excessive risk-taking by market participants, which can be the basis of future financial instability.

Policymakers and central banks must abandon being the driving force of the capital markets. Their behavior has consequences. The permanent bailout attempts and the support of any group prevents the capital markets from performing their very own function of efficient capital allocation.

If the Biden administration refuses to measure its own political success by the performance of the U.S. stock market, this could mean the beginning of a new regime in the capital markets.