US equities in competition with the rest of the world

Dr. René Dubacher

Financial Markets

U.S. stocks hit a relative high last week compared to the rest of the world. EPositive earnings outlook of American blue-chip tech companies and a Corona virus-induced exodus from Asian stocks, were major contributors. The S&P 500 index is up 3% this year despite recent weakness, while the rest of the world is up between 1% and 2%.

U.S. stocks hit a relative high last week compared to the rest of the world. EPositive earnings outlook of American blue-chip tech companies and a Corona virus-induced exodus from Asian stocks, were major contributors. The S&P 500 index is up 3% this year despite recent weakness, while the rest of the world is up between 1% and 2%.

The following chart shows the development of the S&P 500 compared to the MSCI World excluding the USA:

Performance S&P500 vs. world equities ex USA

Looking at the chart, the question arises whether we are in a similar situation to 1999/2000. Then, as now, it was US technology companies that reached very high valuations. The high valuation - late in a business cycle - is accompanied by a clear outperformance of growth stocks ("Growth") versus substance stocks ("Value"); here, too, the values seem to be comparable to 1999/2000.

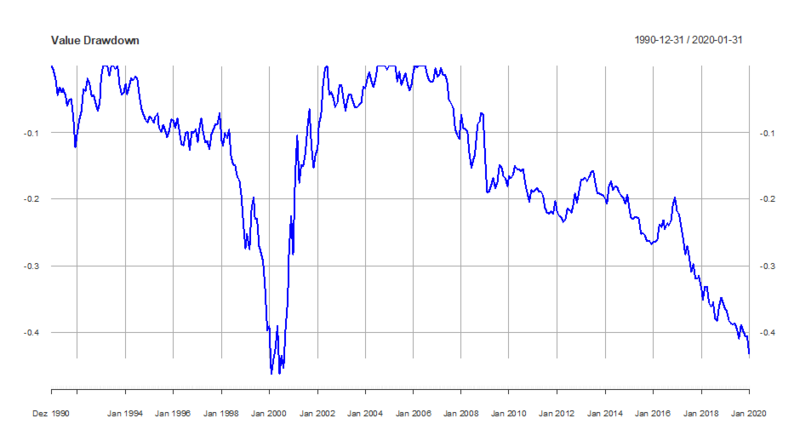

The following chart shows the underperformance of value stocks compared with growth stocks, also known as "drawdown".

Value stocks vs. growth stocks

Although the "party mood" is reminiscent of the euphoria of 1999, there are significant differences. Of course, stocks are expensive, and the S&P 500 is at 22 times expected earnings, its highest level since the last crisis. But in 1999, values were even higher. Back then, the S&P reached 30 times, and the most expensive stock at the time (Microsoft) even reached 60 times earnings.

Skeptics will point to the S&P 500's price-to-sales ratio and enterprise value/cash flow multiples, which are indeed back at levels last seen in 2000. The reason they are higher than the earnings-based multiples is that companies have higher profit margins (in part due to the composition of companies in the index) and interest and taxes are structurally lower.

As reassuring as it may be that the market is not as overvalued today and credit markets are not as unstable as they were 20 years ago, at the same time this tells us little. We may never return to such wild market conditions as we experienced back then. We hope so, because for those of you who have forgotten: Back then, the Nasdaq - after peaking in March 2000 - fell 75% in two years.

So simply stating that stock valuations are not as extreme as they were in 1999 does not protect today's market from a violent correction. But it does argue against the notion of irrational overheating and a resulting meltdown of the financial markets.